COVID-19 just nipped Warren Buffet, one the world’s most revered investors.

Buffet’s Berkshire Hathaway (BRK) posted a record $49.7 billion first quarter loss on Saturday as the conglomerate collapsed all its investments in airlines.

But investors should look past the headline.

Something bigger is happening. The scale of the pandemic is changing how we interact with the world. And not every industry can keep up.

John’s Hopkins University confirms that as of May 3, 1.1 million Americans have been infected with COVID-19. Worse, some 68,500 have died. Suddenly, real world choices that policy makers and corporate managers took for granted only three months ago are necessarily being replaced with digital alternatives.

It has been a trial by fire. Several essential services simply could not be replicated online. Policy makers quickly discovered that sending children to school provides many benefits other than education. Childcare and nutrition can’t be replaced with a laptop and an internet connection. And burdening stressed out parents with the responsibility of teaching fourth grade math didn’t help, either.

On the other hand, many white-collar jobs easily made the transition. The right combination of enterprise software had employees teleconferencing, completing remote teamwork and providing customer sales and service at scale.

In fairness, this digital transformation process has been in the works for a long time. Companies have been moving their infrastructure to the cloud to make better use of a deluge of digital information.

The big idea was to use cloud processing, storage and data analytics to gain business insights and slowly develop new, cost effective business models. The COVID-19 pandemic simply supercharged this transition.

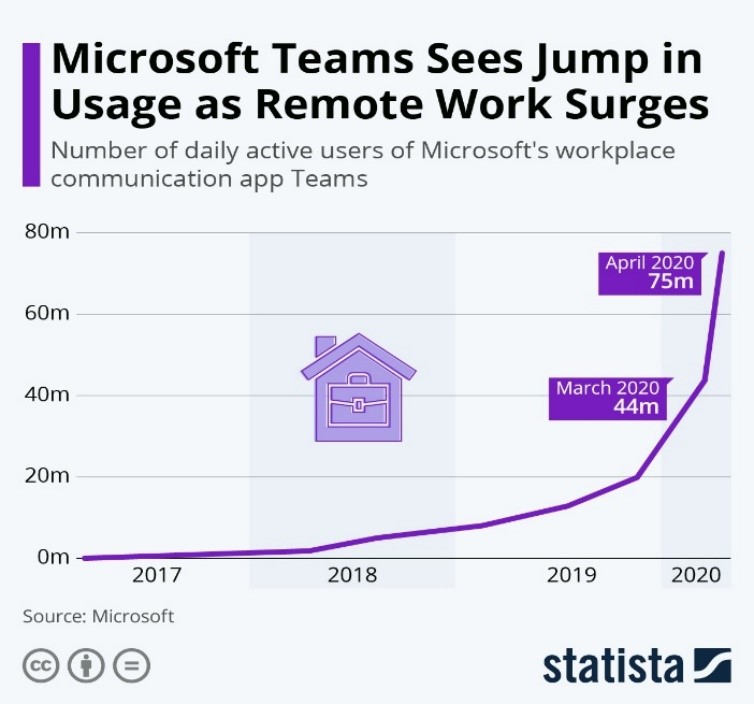

During a conference with analysts last week, Microsoft (MSFT) CEO Satya Nadella said that COVID-19 accelerated two years of digital transformation in only two months.

A corporate press release claimed its Teams teleconferencing software hosted a record 200 million participants in a single day during the quarter. Active daily users surged to 75 million.

Teleconferencing for business negates the need for physical face-to-face meetings. In many cases, participants find online meetings work better than the real thing because it’s easier to exchange and modify information on the fly. Further, everything is conveniently backed up and stored in one digital file.

Microsoft Teams, for example, offers chat, calls, meetings and collaboration in one software package.

A different transition is happening with consumers. Self-quarantines forced people to find an easy-to-use, cross platform alternative to FaceTime on iPhones. Almost overnight, so-called “Zooming” became a verb, and a tiny Silicon Valley company shot into popular culture.

The software, developed by Zoom Video Communications (ZM), is in many ways comparable to Teams. Users can host conference calls, webinars, instant messaging and even make phone calls. The major difference is ease of use. From tweens to Boomers, the Zoom interface makes it dead simple to get an entire family or group of friends together in a video chat within seconds.

At one point, managers at the San Jose, Calif. company said the Zoom platform had 300 million daily active users. Although this claim was later walked back to 300 million meeting participants, it’s important to not lose sight of the underlying trend: People are finding digital alternatives to real world, face-to-face meetings. For travel and hospitality companies, it means the world has changed.

It’s a new reality that Warren Buffet took seriously.

The 89-year-old investor is best known for his disciplined, value investing approach. He takes longer-term positions in companies and sectors that have moats, big competitive advantages that can’t be easily replicated.

In 2017, Berkshire Hathaway added multiple billion dollar stakes in American Airlines (AAL), Delta Airlines (DAL), Southwest Airlines (LUV) and United Airlines Holdings (UAL). Despite multiple bankruptcies and a history of squandered shareholder wealth, Buffet explained that strong industry moats meant it couldn’t get any worse. Better demand and fiscal discipline would lead to a new era of prosperity.

At the time, that bet seemed out of character for Buffet. Today, it looks foolish.

While airline industry executives could not have foreseen the COVID-19 pandemic, they should have understood the forces of digital transformation. They should have been better prepared for a period of slower demand.

Bloomberg reported in March that during the last decade, airline companies spent 96% of free cash flow buying back company stock in the open market. And when the companies were cash flow negative, they borrowed money. Executives always assumed they would be bailed out by rising demand from business and casual travelers.

COVID-19 changed the rule of the game. The virus forced companies and individuals to make do with a digital alternative to a real-world meeting. That trend is only getting started. And travel and hospitality businesses will be the losers. Airlines will likely fare the worst.

Investors should continue to avoid airlines and hospitality businesses in general. They should use weakness ahead to consider positions for companies like Microsoft and Zoom Video. The future is digital — at scale and online.

Best wishes,

Jon D. Markman