Why Mastercard is now set to dominate business transactions

There is a huge opportunity in business-to-business payments that nobody is talking about.

Bloomberg reported Tuesday that Mastercard (MA) agreed to pay $3.2 billion for a digital payments platform based in Denmark. The news barely made a ripple, but the transaction processor is building something big.

Investors should pay attention.

Consumers are spoiled. We have credit cards with chips and Apple Pay on our phones. In most parts of the world, we can swipe or tap a plastic card or our smartphone and buy goods and services instantly. Vendors get the money instantly, too. It’s magic.

Except it’s not. Behind the scenes, robust platforms are working feverishly. In 2018, Visa (V), the world’s largest transaction processor, claimed its network was capable of handling 24,000 transactions per second.

Now contrast that scale and reliability with business-to-business transactions. It’s like time has stood still.

These transactions take an average of 45 days, according to a November 2018 Investor’s Business Daily story. The process involves drafting checks and getting signatures, then mailing (yes mailing) the payment to the vendor. And that’s only the half of it.

Suppliers wait for the check, manually process it, and wait for it to clear before receiving payment.

This process is hopelessly inefficient … and costly. Businesses shell out $2.7 trillion chasing payments. Entire floors in nondescript office towers are devoted to account managers running down missing payments and balancing the books.

Businesses pay a staggering $16-$22 to manually process each invoice, IBD reports.

The big transaction processors have been dutifully assembling the pieces to tackle this problem. Managers at Mastercard declared a war on cash in 2005. Digital transactions are cheaper, easier to track and most importantly, they are many times faster. Ridding the business world of corporate checks is the next logical step.

Mastercard began with payment automation. It built systems infused with artificial intelligence to handle routine payments. People will deal with trickier payments.

The company announced Mastercard Track in September 2018, a cloud based, B2B payment automation platform jointly developed with Microsoft (MSFT). It digitized and organized identity, compliance and payment management. This helps streamline and simplify administrative tasks while reducing cost.

Now Mastercard is upping the ante. Its $3.2 billion acquisition of Nets, a Danish firm with an impeccable reputation in the Nordic region, is a next huge step. The Nets innovative platform has become foundational with banks, merchants, and corporations to simplify digital payments.

It receives transactions, processes and clears them with remarkable speed and reliability. The company claims uptime in 2018 was 99.98%.

The European Commission in 2018 found that Denmark was Europe’s most digitized region. Nets’ scalable network is available to 240 Northern European banks.

Mastercard managers plan to incorporate Nets technologies into its existing mobile wallet, card and bill payment infrastructure.

It’s the latest acquisition is a busy year of buyouts for the New York, N.Y. company. Prior to the Nets deal, Bloomberg notes Mastercard spent $1.1 billion adding Ethoca, an identity fraud company; Vyze, a point of sale company; bill payment specialist Transactis; and Transfast, a cross-border payment firm.

These transactions all serve the same purpose. Mastercard is building a robust network to help businesses send and receive payments faster and with greater transparency.

B2B global payments is a market McKinsey and Co. analysts believe is ripe for disruption. It’s the most vulnerable part of the $1.9 trillion payments segment because there has not been any meaningful innovation in two decades.

Only a handful of companies have the scale, expertise and networks to pull off something this big. And it’s going to happen because it serves the financial interests of government and enterprises, large and small.

Under CEO Ajaypal Singh Banga, Mastercard has been investing aggressively in the payment systems. He expects that all payments, from subway rides to government checks, are going to be fully digital.

Paper corporate checks have outlived their usefulness.

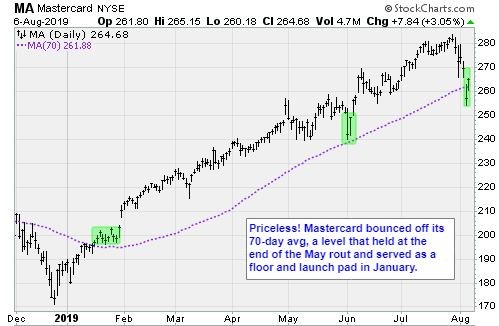

The stock has been under pressure recently as managers invest in new businesses. Shares briefly fell below $260 last week before rebounding. The stock trades at 29.3x forward earnings and 17x sales, for a market capitalization of $270 billion.

Given the prospects for new businesses, like B2B and the scarcity of similar firms, the valuation is reasonable. Mastercard is buyable on pullbacks for growth investors.

Best wishes,

Jon D. Markman