New Boom in Telecommuting Ushered in by COVID-19 Chaos

The entire business world is in the midst of a giant transition.

For plenty of good reasons, remote employment is a growing trend across the corporate world. Though many in the corporate world see the benefits of telecommuting, the adoption has been slow up to this point.

Now the coronavirus — and maturing videoconference technology — is pushing telecommuting to the forefront.

The Los Angeles Times reported Tuesday that Twitter managers are now strongly encouraging most of its 4,800 employees to work from home. Staff in Hong Kong, Japan and South Korea offices will have no choice, due in part to government restrictions on travel. A company blog post notes managers have been working for some time toward a distributed workforce that is increasingly remote.

The push for more telecommuting-friendly jobs has been an ongoing trend. A report from Global Workplace Analytics and Owl Labs found that 34% of telecommuters in the U.S. were willing to take up to a 5% pay cut to continue working remotely.

These employees, on average, were also 29% happier with their jobs, versus onsite workers. Other findings included increased company loyalty and productivity.

In an era of historically low unemployment and labor shortages, expanding the talent pool while also providing employees with the perceived perk a win-win.

It also makes good economic sense. Remote employees typically work more hours for the same pay.

In addition to these usual arguments for telecommuting, the coronavirus outbreak reveals a public safety reason. As fear of the outbreak spreads, conferences all over the world are being cancelled. For many companies, the meetings are simply no longer worth the risk.

Google announced Tuesday that its annual developer conference would be cancelled due to ongoing concerns over the coronavirus. Facebook (FB) and Twitter (TWTR) have said they will not send representatives to SXSW, a giant tech conference held in Austin each year.

Teleconferencing would allow companies to safely send representatives to “attend” these conferences. They also allow said companies to save money. If an employee is telecommuting, there’s no need to pay for their airfare, hotel and food.

The opportunity for investors is found in the technology behind this trend.

Zoom Video Communications (ZM) makes best-in-class, cloud-based software to help companies host business meetings, conference calls, webinars, instant messaging and even phone calls. The platform is robust enough to host 100 interactive video participants, and in excess of 10,000 attendees.

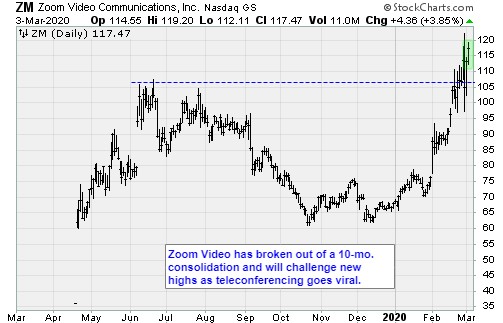

The San Jose, Calif., company offered 20.9 million shares at $36 per share on the Nasdaq exchange last November. It was an immediate success. In the first day the stock zoomed to $62. Three months later it was hovering near $105.

The initial attraction was profitability. Unlike other Silicon Valley companies debuting in 2019, Zoom was already close to making a profit. Its Securities and Exchange S-1 filing revealed $330 million in sales during 2018, with an adjusted profit of 3 cents per share. When accountants finished with the financials, Zoom had a small 7 cent loss.

Most of the firm’s clients have come from larger legacy companies like Cisco (CSCO) and to a lesser extent, Microsoft (MSFT).

Web-based applications such as Webex and Skype for Business were not built with videoconferencing in mind. Their architecture is based on conference call and chat tools, according to the SEC filing.

The limitations of the older code are beginning show up now, especially as companies race to hold entire tech conferences online. Zoom is in the right place at the right time.

Shares have moved to new highs in the wake of the coronavirus, recently trading at $118. Some of this is reflexive. The stock has risen 67% during the past three months alone.

However, another part of the gains can be attributed company transitions started before the virus. The opportunity is real and growing.

Zoom will announce its fourth-quarter financial results after the close Wednesday. The company is expected to earn 7 cents per share on sales of $176.8 million.

There is a good chance positive news is built-in to the current share price. A decline could be in the offing. If that happens, buy the weakness. It will not last.

The future of large parts of employment is remote. Zoom is the most likely company to dominate the field of competing companies.

Best wishes,

Jon D. Markman

P.S. In light of all the frightening news — both real and fake —surrounding the coronavirus outbreak, Dr. Martin Weiss put together an urgent 10-minute video about the true impact COVID-19 could have on your investments and what you should do about it.

If you haven’t seen it yet, I highly recommend you watch it now.