Sharp rebound to Monday smackdown was ingeniously forecast

The extreme -2.5% setback to U.S. markets to kick off this week set off a ton of alarm bells among the sort of quantitative analysts who help us understand current events through the prism of past similar instances.

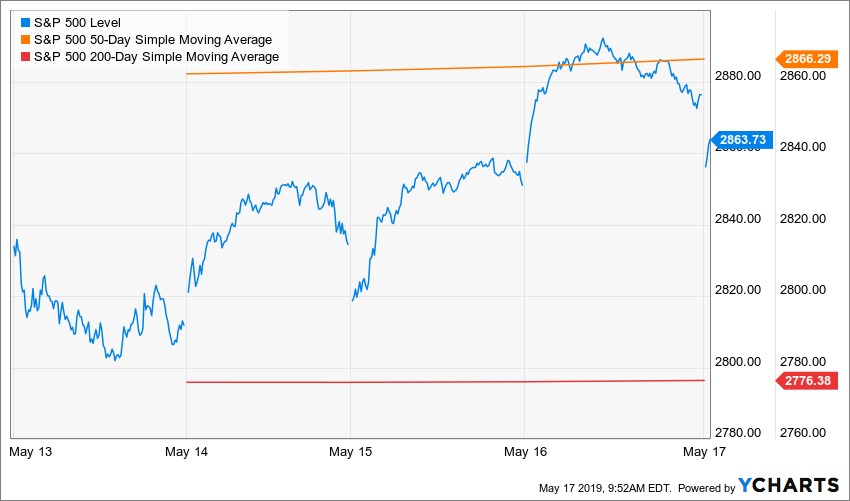

Most of these analysts found that sharp down moves amid an uptrend are usually terminal. In other words, the market tends not to unravel further. They were right, and the markets enjoyed some nice upward action midweek. So, this validated their approach.

Here are a few of better studies I saw:

TGI Mondays

Bespoke Investment Group research showed that since the bull market began in March 2009, there have been 15 prior Mondays when the SPDR S&P 500 (SPY) declined by 2% or more.

- The SPY has been higher on the following trading day 12 out of 15 times for an average gain of 1.01%.

- In the week after 2%+ declines on a Monday, SPY has been up 14 out of 15 times for an average gain of 3.2%. That’s a lot, and it’s in line with what actually occurred Tuesday-Thursday.

The results are even more extreme when you look at 2%+ declines by weekday since 1993, when the SPY began to trade. The day after SPY has declined 2%+ on a Monday has seen an average gain of 1.11%. All other weekdays show basically flat next-day returns.

No wonder the concept of “Turnaround Tuesday” exists.

Shock Days

Jason Goepfert of SentimenTrader.com defines a “shock day” as one in which the result is more than two standard deviations away from what investors have seen over the past year.

By that count, Monday certainly qualified, with a 2.6 standard deviation move in the S&P 500. The drop came within two weeks of the index sitting at new highs, so it’s safe to assume that this volatility caught many off-guard.

Goepfert ran a study of every similar shock day since 1928 — times when the S&P 500 suffered at least a -2.5 standard deviation move within 10 days of it sitting at a multi-year high. There were 26, with the most recent coming Jan. 30, 2018.

It turns out that most were sound and fury, signifying nothing. The average next-week gain was 0.2% and average one-year gain was 11%, which is above average. Only four of them lost a further 5% at any point during the next month.

In other words, there was only a roughly 35% probability of these shock days morphing into anything more sinister. Only one lost more than 10% at any point during the next three months.

Goepfert also looked at just the Nasdaq-100 Index (QQQ). The Nasdaq 100 had just gone from a multiyear high to a 5% pullback in near-record time — certainly one of the fastest major retreats since 1971. On average, it takes at least three weeks to cycle from a peak to a 5% pullback, while this one took just six sessions.

The analyst looked at how the QQQ performed other times it quickly pulled back 5% from a peak. Turns out that, within the next month, just six of the 17 signals lost more than another 5% from the signal date.

This suggests that there was about a 35% probability that the pullback would morph into a correction of at least 10% from the peak.

The average Nasdaq gain over the two months after the signal was +2.4% — and a year later, the instances averaged a big 15.6% gain.

And finally, he looked at the Dow Industrials for instances when the index has moved from within 1% of a high all the way down to a three-month low. Turns out these declines did not typically become more inflamed.

Three months later, the Dow was higher 87% of the time, with a significantly positive average return and excellent risk/reward skew.

There was only a 13% chance that the Dow would lose more than another 10% at any point during the next six months.

So far all this research is proving to be accurate, as the Monday smackdown appears to have been a one-off event that has not led to a severe unwinding of the market.

‘Chimerica’ Vulnerable …

The excellent Bloomberg reporter Tracy Alloway on Thursday reported that her sources believe China is resisting U.S. trade demands because it believes that America’s political system “is in long-term decline” and the Trump administration will cave to special-interest groups as trade tensions cut into profits.

That view came Laban Yu at Jefferies Financial Group, who says the strategy effectively amounts to a bet on “American political decay.” Taking into account U.S. politicians’ ties to special interest groups including farmers and big companies means that China, with its centralized economy and political system, can withstand greater tariff-inflicted pain than America.

“In a bout when two well-matched boxers have arms intertwined, a head-butting strategy will be won by the side who can take the most pain,” Yu wrote in research published this week. “China will test America’s pain threshold with the belief that U.S. politicians are beholden to interest groups.”

On Thursday, less than a week after hiking import tariffs on about $200 billion worth of Chinese products, Bloomberg noted that President Trump appeared to ratchet up his battle with China by moving to curb Huawei Technologies Co.’s access to the U.S. market and American suppliers.

Complicating matters is Trump’s tendency to take credit for rising stock prices, which should theoretically encourage the U.S. president to pursue market-friendly policies, Bloomberg added.

The Republican Party’s business ties were also singled out by Karthik Sankaran, Eurasia Group’s senior strategist, as a potential U.S. vulnerability. The analysts at Eurasia Group see China and America forming a single trading bloc they call “Chimerica.”

“Trump’s problem is that if Chimerica as an economic system is the union of Chinese labor and American capital, then it’s really hard to hurt Chinese labor without hurting American capital, which is hard for the self-described party of American capital,” he wrote on Twitter.

Poor Sentiment is Good News For Bulls

And now let’s finish with two positive data updates from Jason Goepfert of SentimenTrader.com. First …

“Every month, the U.S. Treasury releases general details about how various parties transacted in U.S. markets. The just-released data cover transactions through March, and it continued a recent trend: foreigners have been heavy sellers of stocks. Non-U.S. entities sold an average of $17 billion worth of stocks each month over the past year, by far the most in 30 years.

“That amounts to about 0.05% of total U.S. market cap per month, which doesn’t sound like much. But relative to other readings, it’s still the most ever.

“Yet foreigners are no better at market timing than anyone else. Extremes in their buying and selling tending to coincide reciprocally with extremes in U.S. stock indexes, suggesting their current pessimism should be a good long-term sign.”

* … And here is a second item from Goepfert:

“Individual investors are taking the recent sell-off seriously. The last couple of weeks have seen some of the largest pre-market losses since the financial crisis — helping to trigger an exodus from an array of equity funds. A drop in some of the most recent surveys isn’t unexpected, but the drop in the AAII one is severe. Bears outnumbered bulls, driving the Bull Ratio (Bulls / (Bulls + Bears)) below 44% …

“The average Bull Ratio has been closer to 58%. That makes the current reading extreme not only on an absolute basis, but also relatively.

“Future returns in the S&P 500 when the Bull Raito is below 44% has tended to be quite positive for stocks, especially over the next three to six months. SentimenTrader.com studies show that when that ratio appears in bull markets, the average gain over the next two months is 4.1% and +8.4% for six months.”

Best wishes,

Jon D. Markman