Surprise: Best New Online Retailer Might be Facebook

The growth of online shopping is probably peaking right now. That’s bad news for shareholders of many e-commerce companies.

On Saturday, Adobe Inc. (Nasdaq: ADBE) released the first look at online Black Friday sales. Shoppers spent $9 billion, up 21.6% from a year ago. Unfortunately, the comparisons to years past will get more difficult moving forward.

To be clear, the current state of e-commerce is robust. The global pandemic pushed millions of new costumers online. By all accounts, they became too comfortable too quickly.

The Adobe Digital Insights survey revealed that 41% of shoppers started their holiday buying well ahead of Black Friday. Analysts also noted that consumers are likely to continue spending online throughout the holiday season as they mix gift buying with necessities and nonessential items.

The transition online illuminated many smaller e-commerce businesses that had been hiding in the shadow of Amazon.com, Inc. (Nasdaq: AMZN). As they emerged, the new attention produced big gains for shareholders. Overstock.com, Inc. (Nasdaq: OSTK), Farfetch Ltd. (NYSE: FTCH), Wayfair Inc. (NYSE: W) and Mercadolibre, Inc. (Nasdaq: MELI) shares are up 907%, 418%, 185% and 164%, respectively, in 2020.

However, the global rollout of COVID-19 vaccines means many shoppers will soon head back to brick-and-mortar stores. Online sales growth should slow, perhaps dramatically. Share prices for some e-commerce companies are likely to follow.

That’s why investors need to be looking in unconventional places. One of the best potential new places to look is the social media giant Facebook, Inc. (Nasdaq: FB).

Aside from being a place where we connect with friends and family, the site is building a new e-commerce platform with the potential to produce billions in new sales. Those gains will drive the share for the foreseeable future. The good news is that so far, investors are none the wiser.

Related Post: Facebook proves Big Tech’s Scale Reigns Supreme

The San Francisco-based company is engrained in our social consciousness. Members use it because it is where friends and family live online. Leaving the community makes keeping in touch in a digital world untenable. That’s why membership, to the chagrin of critics, continues to grow despite scandals over privacy, censorship and the management of the business.

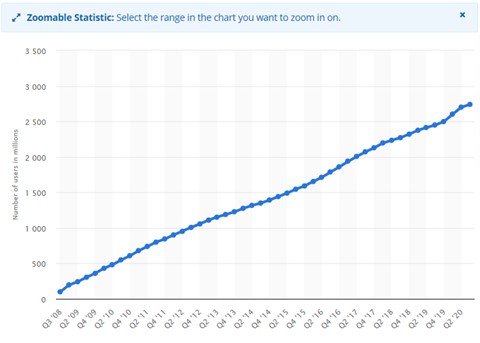

Through the first quarter of 2020, Statista reported that 2.6 billion members login at least once a month. That figure jumps to 3 billion with the addition of core properties, WhatsApp, Instagram and Facebook Messenger.

The major breakthrough of this opportunity is managers are now in the process of monetizing these platforms beyond advertising.

Facebook Shops, introduced in May, will help members across Facebook and Instagram create contained, end-to-end e-commerce stores. It’s not hard to imagine members sharing photos of products on Instagram and Facebook Groups, then completing online sales in Shops using Facebook Pay, its digital payment processor.

The last part is key. Facebook managers intend to keep member payment credentials inside Pay to help with portability between Facebook and Instagram. This means no annoying logins or hand-offs to third-party processors to detract from the experience. It also means complete control of the user experience.

Through the first half of 2020, more than 80 million businesses used Facebook to connect with customers. That number is certain to grow as Facebook managers make it even easier to build storefronts and process payments. And the growth of this new revenue stream should provide several years of favorable comparable numbers because sales are beginning from a very low point.

Related Post: Google and Facebook Will be the Last Ad Platforms Standings

When Facebook reported financial results on April 29, 98.3% of the reported $17.4 billion in sales came from advertising.

It may seem counterintuitive to close out long positions in emerging online retailers like Farfetch, Wayfair and Mercadolibre in favor of Facebook. It feels like trading something for nothing. The reason this trade makes sense is sales growth and the way momentum stocks are valued in the marketplace.

Slower growth is a death knell for momentum issues. It means much lower prices.

Adobe Digital Insight analysts crunched through billions of data points across 100 million product SKUs. The data is bullish overall for online sales moving forward, but that will not be enough for most high-flying e-commerce stocks.

Savvy investors should strongly consider taking profits on some of these momentum stocks. Then, they should look at potential future e-commerce winners like Facebook.

Best wishes,

Jon D. Markman