U.S.-China dispute: A struggle for 21st-century dominance

Stocks clanked again over the past week in a series of volatile sessions in which sentiment waxed and waned and fretted and cheered over the loop-de-loop path of U.S.-China trade talks.

Topping the new high list at the close of the week was spirits maker Diageo (DEO). How appropriate.

Also on the list were Red Hat (RHT), Atlassian (TEAM), Formula One Group (FWONA), J.M. Smucker (SJM) and Fair Isaac (FICO) — not exactly a star-studded group.

The back-and-forth in markets showed investors struggling to make sense of the U.S. and China trade negotiations. The last time trade talks went down to the wire was the renegotiation of NAFTA, which was ultimately resolved in a phone call between leaders.

It’s the cliffhanger ending that satisfies a reality TV veteran’s lust for drama. A blockbuster climax in which the U.S. backs down but saves face would not be a surprise.

No matter how the final negotiations are spun, I think it’s important for Americans to realize that there is much more than simply tariffs and trade at stake. The world’s two largest economies are sparring over commercial hegemony.

On the surface, it’s too easy to see the dispute as a finite set of squabbles. But it’s really about technological and financial dominance over the next few decades.

Jack Ablin of Cresset Capital in Chicago observes that the U.S. is handicapped in this effort. For example …

- Our nation’s ethical policy framework sets guidelines on U.S. stem cell research and cloning. China is unconstrained by such measures, he notes.

- The U.S. government cannot own companies directly, as China does, to help drive research outcomes in technology, healthcare and alternative energy. Indeed, Jack points out that China’s alternative energy initiatives helped them dominate the solar industry: The country generates more than 130 gigawatts of electricity using solar power, double the U.S. output.

Given the breadth and depth of the issues between the two nations, Jack argues that America’s dispute with China cannot be resolved quickly or easily. In fact, he can envision a scenario in which certain tariffs remain in place indefinitely despite an interim agreement.

A further breakdown in talks would take its toll on equity markets.

Whether an ensuing pullback would be an opportunity or a threat would depend on liquidity trends. For now, Jack’s research shows that liquidity levels are fine, as evidenced by lenders’ willingness to extend credit.

If markets reel, it’s fair to take comfort in the White House’s desire to spur a rally going into the 2020 election season. The president has many levers to pull in fiscal and monetary policy to make that happen. And he might have to pull them all.

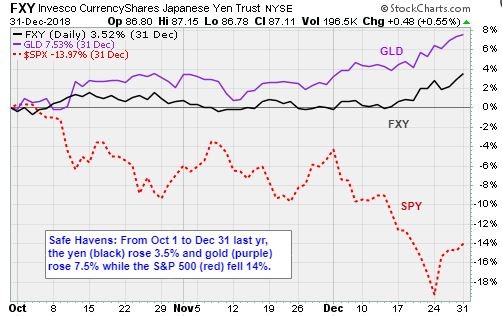

Gold, Yen: Safe Havens in a Trade Storm

The rally in safe-haven trades like gold and the yen amid the global sell-off suggests that investors are quite concerned about a renewed escalation of trade tensions.

Irrespective of how trade negotiations eventually play out, analysts at Capital Economics think the yen and gold will advance this year as the U.S. economy slows sharply and the rest of the world remains weak.

Since the president’s late-Sunday tweet, triggering a sharp sell-off in global equities, the price of gold has edged higher and the Japanese yen has rallied against the U.S. dollar.

But that’s not the end of the story.

Even if the U.S. and China reach a deal, risky assets like equities may continue to fall out of favor as a result of a slowdown in the global economy. If so, then the yen-gold trade — buyable through the ETFs Invesco CurrencyShares Japanese Yen (FXY) and SPDR Gold (GLD) — will have more running room.

CapEcon analysts note that over the past 10 years, during stretches when the S&P 500 has fallen by at least 5%, the Japanese yen has on average appreciated by 4% against the U.S. dollar, while gold has risen by nearly 2%.

In addition to safe-haven demand, gold and the yen ought to benefit from looser monetary policy in the United States. The analysts note that since gold bears no interest, it tends to rise when Treasury yields fall, as they are on track to do this year. Technically gold has upside to at least the $1,400/ounce area this year, which would be a 9% advance from the current level around $1,285/ounce.

*

The fake-outs, dekes and feints in this episode of the presidential reality show are even shakier than usual.

At the moment, this month has the distinct aroma of last October, which was a drag. But my friend Tom McClellan — one of the world’s leading technical analysts — has an optimistic view.

Here is an upbeat note from him that he sent Wednesday night:

“If you want … . a really bullish argument, consider [we] are in the third year of a presidential term, which is historically a bullish period for stocks. And the prior period showing the strongest resemblance to the current market action was “President Clinton’s first term in 1995 … a long, linear, low-volatility uptrend. There was the traditional May dip in 1995, with the S&P 500 dropping 1.7% in just 3 days to a low on May 19, 1995.

“Afterward, the S&P 500 went back to screaming higher, on the same upward slope that had existed before. This week is another three-day drop, albeit earlier in the month of May than the 1995 episode, but still basically in the character of that May 1995 dip.

“So if we really are replaying the 1995 script, then the uptrend should resume itself. That is the big bullish argument.”

OK then. Hope that works out. We’ll know soon enough.

Best wishes,

Jon D. Markman